From electronics giants to mall-fashion staples and quirky home décor chains, Canadian retailers shaped Saturday errands, teenage jobs, and back-to-school rituals. Then, seemingly overnight, they were gone, signs pulled down, shelves emptied, and loyal shoppers left wondering what happened. Here are 21 Canadian retail stores that disappeared overnight.

Target Canada (2015)

Target arrived with goodwill, bright stores, and ambitious timelines, then struggled with inventory accuracy and price perception. Shoppers found too many empty shelves and not enough U.S.-style “Tar-zhay” deals, while distribution centers battled data and logistics kinks. With losses mounting, the company put its Canadian subsidiary into court protection and announced a full wind-down, shuttering 133 stores and two distribution centers. Tens of thousands of jobs disappeared in months, landlords scrambled to re-tenant massive boxes, and liquidators cleared brand-new fixtures. The abrupt exit reset expectations around large U.S. entries: great brand heat is not a substitute for supply-chain execution, localized pricing, and realistic ramp-up assumptions.

Sears Canada (2017)

For decades a department-store anchor, Sears Canada couldn’t pivot fast enough from catalog legacy and mall traffic decline to e-commerce agility and specialty competition. Private-label strength and appliances once drew loyal traffic, but store refreshes lagged, and merchandising skewed older as fast fashion ate share. After attempting store closures, asset sales, and brand licensing, the chain entered liquidation. Appliances and fixtures went first; softlines followed. Malls lost a major anchor, smaller brands lost footfall, and service networks tied to warranties scrambled. The collapse underscored that debt-burdened, legacy department stores cannot fund reinvention while foot traffic erodes and digital customer journeys leap ahead.

Future Shop (2015)

Owned by Best Buy, Future Shop was once a powerhouse in consumer electronics with aggressive promos and knowledgeable sales staff. As omnichannel expectations rose, running two near-identical banners became inefficient. Best Buy closed all Future Shop locations overnight, converting many to Best Buy and shuttering the rest. Consumers suddenly found red signage gone, warranties migrated, and flyers replaced. Staff faced rehiring processes at converted stores or layoffs where closures stuck. The episode showed consolidation economics: duplicated leases, marketing, and inventory planning are hard to justify when margins narrow and online price transparency compresses promotional calendars.

HMV Canada (2017)

Music retail shifted from physical ownership to streaming, with DVDs following a similar path to digital. HMV tried exclusive merch, vinyl revivals, and pop-culture accessories, but rent obligations and falling unit sales outpaced margin improvements. When the numbers no longer supported its store fleet, HMV entered receivership, and locations liquidated quickly, some replaced by other pop-culture chains. The abrupt end highlighted a structural reality: when core consumption moves to subscriptions, square footage must deliver higher-margin collectibles or experiences, consistently. If those adjacencies underperform or arrive too late, even a beloved brand cannot carry the rent.

Rogers Video (2012)

Rogers Video was a familiar neighborhood stop for DVDs and games until streaming, cable VOD, and digital downloads flipped consumer behavior. As title windows shortened and home bandwidth improved, physical rentals fell off. Rogers consolidated, then closed remaining stores, often integrating some functions into The Source or promoting alternative content services. Prepaid gift cards, membership perks, and in-store promotions became stranded assets for consumers. The exit made clear how rapidly video revenue migrated to platforms, turning once-busy Friday night lineups into empty aisles, and leaving landlords searching for tenants suited to smaller, more flexible footprints.

Blockbuster Canada (2011)

The Canadian arm’s troubles accelerated after its U.S. parent’s bankruptcy. Even with Canadian operations initially seen as stronger, the industry’s tidal shift to streaming overwhelmed the model. Gift cards and memberships became a flashpoint when receivership halted redemptions, frustrating customers. Stores liquidated swiftly, selling racks, candy fixtures, and branded signage along with discs. The brand’s cultural ubiquity could not offset relentless format change. For landlords, it meant a wave of small-box vacancies in suburban plazas; for competitors, it opened the door for quick-service, fitness, or specialty food, formats better aligned with everyday traffic than media ownership.

BiWay (2001)

BiWay served value-seeking families with no-frills basics across urban and suburban neighborhoods. The chain struggled with supplier terms, competition from expanding big-box formats, and thin margins. After financial strain and attempts to reorganize, stores closed and signage disappeared quickly. Years later, plans for a modern revival surfaced in limited form, but the original fleet and model had already exited. The closure marked an early warning that off-price and dollar concepts needed sharper sourcing, faster turns, and disciplined private label to survive as global retailers and warehouse clubs taught shoppers to expect deep value, every day.

SAAN Stores (2008)

SAAN built a following in smaller markets with apparel, workwear, and home basics. As retail consolidated and giants pushed into secondary towns, SAAN’s assortment and store refresh cycles couldn’t keep pace. Rising freight, tougher vendor credit, and aging store environments compounded the pressure. A restructuring wasn’t enough; liquidation followed, and communities that relied on SAAN for accessible basics lost a convenient option. The aftermath revealed how fragile rural and small-town retail ecosystems can be when one anchor supplies essentials across categories. Replacing it isn’t simple when chains seek dense, high-income catchments for new leases.

Bargain Harold’s (2005)

A well-known discount chain in Ontario, Bargain Harold’s thrived in the ’80s and early ’90s on closeouts and sharp price points. Over time, supply chains professionalized, dollar formats standardized, and competition multiplied. Without the scale and sourcing muscle of national rivals, margins compressed. Lease renewals and fixture upgrades were difficult to justify against declining traffic. The brand wound down quietly, leaving small urban storefronts to be carved into service tenants or independent convenience concepts. Its departure showed how discount retail isn’t just about low prices; it’s about resilient, predictable pipelines of goods and a repeatable in-store experience.

XS Cargo (2014)

XS Cargo specialized in liquidation buys and opportunistic deals, selling everything from small appliances to camping gear. When consumer demand is inconsistent and sourcing depends on distressed inventory, cash-flow timing becomes critical. After supplier pressure and tougher competition, XS Cargo sought protection and quickly liquidated its stores. Shoppers who had come for surprise finds encountered store-closing signs and bulk fixture sales. The collapse illustrated the volatility of a model built on opportunistic purchasing: it can deliver treasure-hunt excitement, but without disciplined inventory turns and a backstop of stable categories, a few bad cycles can end the game suddenly.

Jacob (2014)

Jacob was a familiar mall apparel brand balancing office basics with seasonal trends. As fast fashion accelerated design cycles and price competition, Jacob wrestled with shrinking margins and mounting lease commitments. Efforts to refocus on core customers and improve merchandising cadence weren’t enough to offset traffic declines. The chain filed for protection, then moved to full liquidation, with loyal shoppers snapping up final runs of suiting and dresses. The exit demonstrated how mid-market apparel, squeezed between luxury and deep discount, needs speed, data-driven buys, and digital storytelling. Without those, even strong brand recognition won’t save a lease-heavy fleet.

Le Château (2020, stores closed)

Long synonymous with occasion wear and going-out styles, Le Château faced the double hit of e-commerce rivals and the pandemic’s blow to events. The company sought creditor protection and closed all stores, later reviving the label online under new ownership. For mall operators, the loss meant another fashion vacancy just as traffic was fragile. For customers, it ended the tradition of last-minute dress or suit runs before weddings and parties. The shutdown underscored event-dependent apparel risk: a sudden demand shock can break cash cycles if inventory is fashion-forward, seasonal, and bought far in advance.

Danier Leather (2016, stores closed)

Danier combined house-brand design with leather craftsmanship, selling jackets, handbags, and accessories at accessible price points. Shifts toward lighter fabrics, athleisure, and online comparison chipped away at sales while fixed costs remained high. After attempts to restructure, the company liquidated stores; the brand later lived on through licensing and limited channels. The abrupt closures left premium inventory to be sold off at steep discounts, eroding perceived value. The lesson was clear: material-specific specialists must evolve into lifestyle brands or flexible DTC operators, or risk being cornered when trends rotate away from their signature category.

Bowring (2019)

Home décor and tabletop retailer Bowring relied on gift-giving seasons and wedding registries. As big-box players expanded assortments and online marketplaces undercut margins, traffic thinned. After ownership changes and efforts to streamline, Bowring stores wound down alongside related banners. Mall corridors that once featured ceramic place settings and glassware displays quickly hosted “Everything Must Go” signs. The closure highlighted how registry economics moved online, where breadth, reviews, and easy returns dominate. Specialty home stores needed distinctive private label or experiential services to survive; without them, rent and inventory carrying costs became untenable.

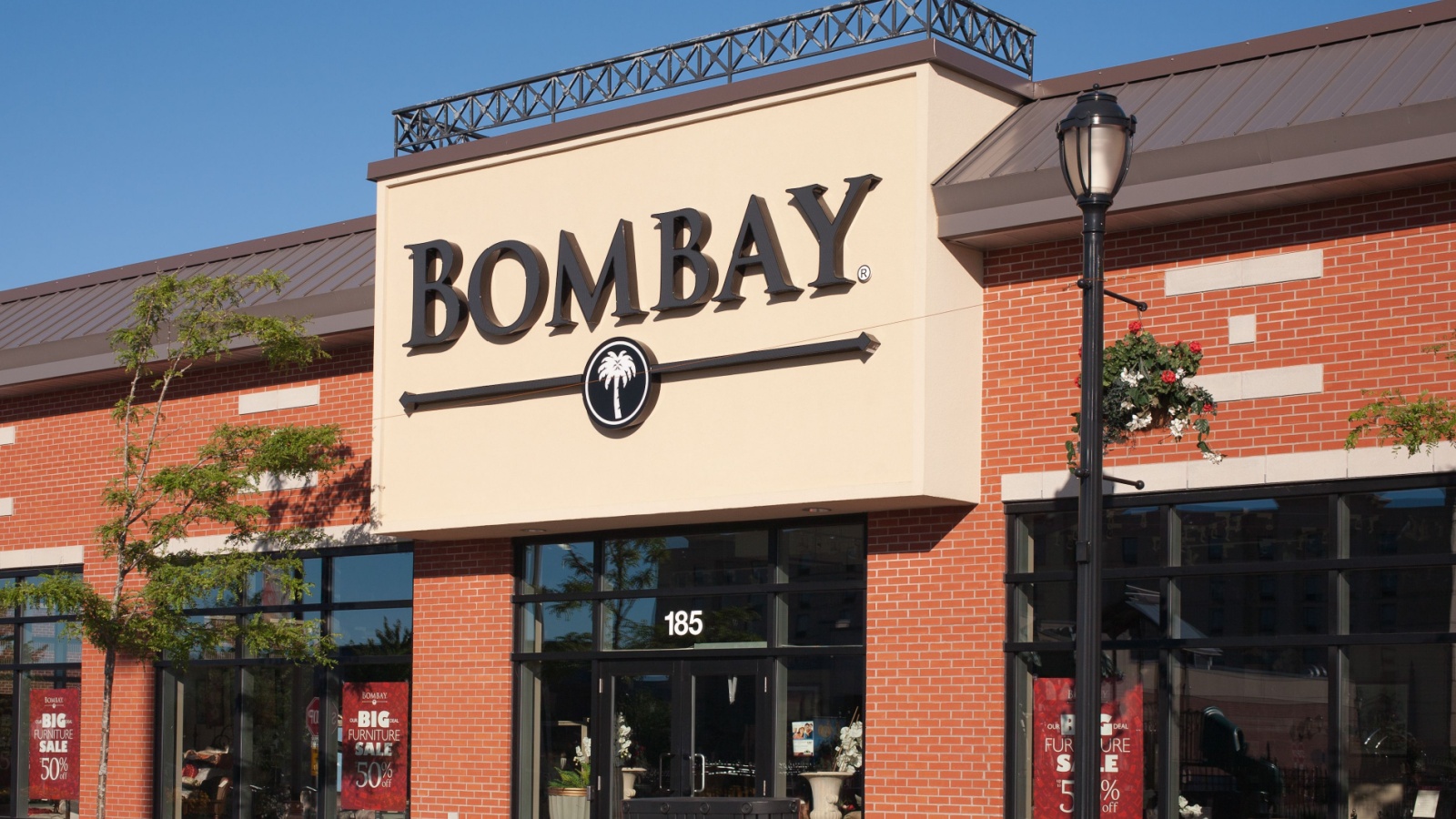

Bombay Company (Canada) (2018–2019)

Bombay’s classic furniture and décor aesthetic resonated for years, but consumer tastes shifted toward modern lines, while shipping costs and price transparency tightened margins. Canadian operations reduced footprints and explored e-commerce, yet store performance lagged. Liquidations followed, sometimes in tandem with Bowring. The exit freed sizable retail boxes for home improvement or athletic tenants better aligned with traffic. For suppliers, it meant rehoming private-label capacity. The brand’s departure showed how furniture retail needs agile sourcing, flat-pack innovation, and digital visualization tools; absent those, overheads overwhelm even well-known banners during a style pivot.

Black’s Photography (2015)

A household name for prints and photo finishing, Black’s faced the smartphone era’s crushing math: fewer prints per person, more instant sharing, and razor-thin margins on hardware. Efforts to push canvas wraps, photobooks, and tech accessories helped, but couldn’t offset rent and labor. Parent-company restructuring led to a decision to close all stores, later experimenting with online-only offerings. Consumers lost a convenient place for quick passport photos and same-day enlargements, and landlords lost a service tenant that once drove weekday traffic. The outcome reinforced how digital habits can erase the base volume needed to fund specialty storefronts.

Grand & Toy (Retail Stores Closed 2014)

Office supplies migrated to B2B contracts and e-commerce, reducing the need for high-street stores. Grand & Toy kept its commercial business but closed remaining consumer-facing locations, redirecting customers online. The shift happened quickly, with signage removed and fixtures sold, even as the brand endured in procurement portals. It was a clean demonstration of channel optimization: when foot traffic’s role diminishes, the right move is to invest in delivery logistics and account services rather than retail leases. For shoppers, it meant no more last-minute toner runs at lunchtime; for cities, another vacancy to backfill.

Pier 1 Imports Canada (2020)

Pier 1’s curated décor, pillows, and seasonal goods once drew regular browse-and-buy trips. But competition from big-box private label and online marketplaces eroded price authority. The pandemic’s shock cut traffic and complicated inventory turns. Corporate bankruptcy led to the decision to close all stores, with Canadian locations liquidating alongside U.S. stores. Some intellectual property later reappeared online, but the warm, fragrance-filled store experience vanished from retail corridors. The exit emphasized that specialty home retailers must pair unique design with agile supply chains and data-driven replenishment, or risk being out-assorted and out-priced by faster players.

Payless ShoeSource Canada (2019)

Known for family footwear at wallet-friendly prices, Payless faced rising competition from fast fashion, off-price chains, and e-commerce. Debt loads and an aging store base compounded pressure. After earlier restructurings, the company shut all North American stores, including Canada, in a rapid liquidation. The brand later explored online comebacks, but the nationwide physical presence was gone. The closure left value-oriented gaps in many smaller markets and strips where Payless had been a reliable co-tenant. The playbook takeaway: when assortment feels commoditized and store experiences stagnate, promotional cadence alone can’t rescue traffic or margin.

Nordstrom Canada (2023)

Nordstrom’s Canadian experiment brought polished service and curated brands to urban malls, plus off-price Nordstrom Rack. Despite strong brand equity, sales targets didn’t justify the scale amid high occupancy costs and a tricky retail climate. The company elected to wind down Canadian operations via court-supervised proceedings, liquidating six full-line stores and several Racks. For shoppers, return policies tightened during wind-down; for malls, it meant replacing a premium anchor during a period of shifting luxury demand. The exit showed that even well-executed formats struggle without sufficient market density, supplier terms, and long-run break-even timelines.

Bed Bath & Beyond Canada (2023)

A destination for dorm, wedding, and home basics, Bed Bath & Beyond relied on big assortments, coupon-driven traffic, and national brands. As private-label initiatives faltered and supply-chain challenges hit, out-of-stocks rose and shopper trust slipped. The parent’s financial strain accelerated store closures; Canadian operations shut down through court proceedings, and liquidations moved quickly across the fleet. Consumers rushed for clearance deals while registries were redirected or canceled. The collapse underscored how home-category retailers must balance breadth, dependable availability, and sharp everyday pricing; once that triangle breaks, coupons can’t bridge the confidence gap for long.

21 Products Canadians Should Stockpile Before Tariffs Hit

If trade tensions escalate between Canada and the U.S., everyday essentials can suddenly disappear or skyrocket in price. Products like pantry basics and tech must-haves that depend on are deeply tied to cross-border supply chains and are likely to face various kinds of disruptions

21 Products Canadians Should Stockpile Before Tariffs Hit