Car payments in Canada have reached record highs in 2026, as longer loan terms, rising interest rates, and rising vehicle prices reshape how Canadians finance vehicles. Many buyers commit to monthly payments that seem manageable at first but become burdensome over time. At the same time, smarter financing strategies and better vehicle choices can significantly reduce long-term costs. Here are 23 car payments Canadians regret most (and the deals that actually make sense in 2026).

Long-Term Loans on Entry-Level Sedans

Many Canadians regret financing entry-level sedans over extended loan terms such as seven or eight years. While monthly payments appear lower, the total cost increases significantly due to interest accumulation. These vehicles also depreciate quickly, meaning owners often owe more than the car’s value for several years. This creates limited flexibility if they want to sell or upgrade. A more sensible approach in 2026 is choosing shorter loan terms or slightly higher monthly payments to reduce overall interest. Buyers who prioritize total cost over monthly affordability tend to make better long-term decisions and avoid being locked into outdated vehicles.

Financing Luxury Vehicles Without a Stable Income

Luxury vehicles come with higher purchase prices, insurance costs, and maintenance expenses, which many Canadians underestimate. Financing these vehicles without a stable income often leads to financial strain when unexpected expenses arise. Monthly payments can quickly become difficult to manage, especially as interest rates remain elevated. Many buyers regret prioritizing status over practicality. A better approach is waiting until income comfortably supports both payments and ongoing costs. In 2026, choosing reliable mid-range vehicles with strong resale value often provides a more balanced financial outcome without long-term stress.

Zero-Down Deals With High Interest Rates

Zero-down financing deals can be appealing, but they often come with higher interest rates that increase the total cost of ownership. Canadians who choose these options may end up paying significantly more over time. Without an initial down payment, loan balances remain higher, and interest accumulates faster. This can also lead to negative equity early in the loan. A smarter alternative is making even a modest down payment, which reduces both monthly payments and interest costs. In 2026, buyers are increasingly recognizing that upfront contributions lead to better long-term value.

Leasing Without Understanding Mileage Limits

Leasing can seem affordable, but many Canadians regret agreements that include strict mileage limits. Exceeding these limits results in additional charges that can quickly add up. Drivers who underestimate their usage often face unexpected costs at the end of the lease term. Leasing works best for those with predictable driving habits. In 2026, buyers who prefer flexibility are often better off financing or choosing leases with higher mileage allowances, even if monthly payments are slightly higher.

Buying Electric Vehicles Without Charging Access

Electric vehicles are growing in popularity, but some Canadians regret purchasing them without reliable home or nearby charging options. Public charging infrastructure continues to expand, but access can still be inconsistent in certain areas. This leads to inconvenience and added costs. Buyers who plan ahead and ensure charging availability tend to have better experiences. In 2026, EV ownership makes the most sense when charging is convenient and integrated into daily routines.

Financing Used Cars at High Interest Rates

Used cars can be a cost-effective choice, but high interest rates often reduce their value advantage. Canadians who finance used vehicles at elevated rates may pay nearly as much as they would for a new car. Older vehicles may also require more maintenance, increasing overall costs. A better strategy is to compare the total cost rather than the purchase price alone. In 2026, certified pre-owned vehicles with lower rates often provide better value and reliability.

Rolling Negative Equity Into New Loans

Many Canadians trade in vehicles before paying off existing loans, rolling remaining balances into new financing agreements. This increases total debt and monthly payments, often leading to long-term financial strain. Negative equity can accumulate quickly, making it harder to break the cycle. A smarter approach is paying down existing loans before upgrading. In 2026, buyers who avoid rolling debt into new loans maintain better financial control and flexibility.

High Monthly Payments on Pickup Trucks for City Use

Pickup trucks are popular in Canada, but many urban drivers regret high monthly payments for vehicles they do not fully utilize. Fuel costs, insurance, and financing payments can be significantly higher than those for smaller vehicles. Buyers often overestimate their need for utility. In 2026, compact SUVs and hybrid vehicles will offer more practical alternatives for city driving, reducing both upfront and ongoing costs while maintaining versatility.

Ignoring Insurance Costs During Financing

Many Canadians focus on monthly loan payments without considering insurance costs, which can vary significantly depending on the vehicle. High-performance or luxury models often carry higher premiums, increasing total expenses. This can make an otherwise manageable payment difficult to sustain. A better approach is factoring insurance into the total cost before purchasing. In 2026, buyers who consider all expenses upfront make more informed decisions.

Choosing Features Over Reliability

Some buyers prioritize features such as advanced technology or luxury interiors over long-term reliability. This can lead to higher maintenance costs and reduced resale value. Canadians often regret paying more for features that do not significantly improve daily use. In 2026, vehicles known for reliability and lower ownership costs provide better long-term value than those focused primarily on features.

Skipping Pre-Purchase Inspections on Used Cars

Skipping inspections to save time or money can lead to costly repairs later. Many Canadians regret purchasing used vehicles without understanding their condition. Hidden issues can increase ownership costs significantly. A pre-purchase inspection provides valuable insight and helps avoid unexpected expenses. In 2026, this step remains essential for making informed decisions in the used car market.

Financing Add-Ons That Inflate Loan Amounts

Dealership add-ons such as extended warranties, protection packages, and accessories are often rolled into financing agreements. While they may seem useful, they increase the total loan amount and interest paid. Canadians frequently regret these additions when they realize the long-term cost. A better approach is to evaluate each add-on carefully and pay separately if needed. In 2026, minimizing unnecessary extras helps keep financing manageable.

Buying Brand-New Instead of Nearly-New

Many Canadians regret buying brand-new vehicles when nearly-new options offer better value. New cars depreciate quickly within the first year, which means buyers lose a significant portion of value almost immediately. Financing a brand-new vehicle also increases monthly payments and total interest paid. In contrast, lightly used or certified pre-owned vehicles often provide similar features at a lower price. In 2026, supply conditions have improved, making nearly-new vehicles more accessible than before.

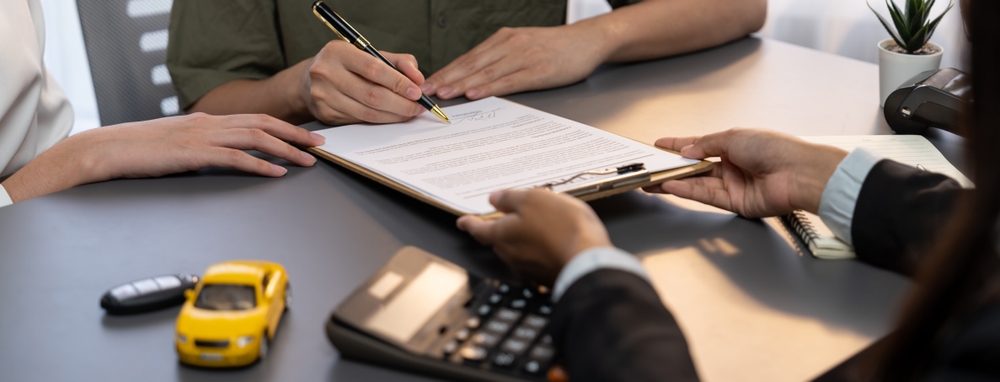

Ignoring Total Loan Cost

Focusing only on monthly payments is one of the most common mistakes Canadians make when financing a vehicle. Many buyers agree to terms that seem affordable each month but result in a much higher total cost over time. Interest rates, loan length, and additional fees all contribute to the final amount paid. In 2026, with higher borrowing costs, this issue has become even more significant. Buyers who calculate the full loan cost before committing are better positioned to avoid regret. Understanding the complete financial picture leads to more informed and sustainable decisions when purchasing a vehicle.

Choosing Variable Rate Financing

Variable-rate financing can appear attractive initially due to lower starting rates, but it carries risk when interest rates rise. Many Canadians who selected variable rates in previous years now face higher payments than expected. This unpredictability can strain budgets, especially during economic uncertainty. Fixed-rate financing provides stability and makes long-term planning easier. In 2026, many buyers prefer predictable payments even if the initial rate is slightly higher. Choosing stability over short-term savings often results in better financial outcomes and fewer surprises throughout the loan term.

Overestimating Resale Value

Some buyers justify higher payments by assuming strong resale value in the future, but this expectation does not always hold. Market conditions, mileage, and vehicle condition all affect resale prices. Canadians who rely on optimistic estimates may end up with less value than expected when selling or trading in. This can create financial gaps and increase overall costs. In 2026, focusing on realistic depreciation rather than assumptions helps buyers make more practical decisions. Choosing vehicles known for consistent resale performance reduces risk and improves long-term value.

Financing Through Dealership Without Comparison

Many Canadians accept dealership financing without comparing rates from banks or credit unions. While convenient, dealership financing may not always offer the best terms. Interest rates and conditions can vary significantly depending on the lender. Buyers who do not explore alternatives may pay more over time. In 2026, comparing financing options has become easier through online tools and pre-approvals. Taking time to evaluate different offers often leads to lower interest rates and better overall terms, reducing total ownership cost.

Buying More Cars Than Needed

Choosing a vehicle that exceeds actual needs is a common regret among Canadian buyers. Larger or more expensive vehicles come with higher payments, fuel costs, and maintenance expenses. Many buyers justify these purchases based on occasional use rather than daily requirements. In 2026, practical decision-making has become more important as costs rise. Selecting a vehicle that aligns with everyday use helps reduce financial strain. Smaller, efficient vehicles often provide better long-term value without sacrificing functionality for most drivers.

Ignoring Fuel Costs in Financing Decisions

Fuel costs are often overlooked when calculating total vehicle expenses. Larger vehicles or those with lower efficiency can significantly increase monthly spending beyond loan payments. Canadians who focus only on financing may underestimate these ongoing costs. In 2026, with fuel prices remaining unpredictable, efficiency plays a major role in affordability. Buyers who consider fuel consumption alongside financing make more balanced decisions. Choosing hybrid or efficient models often reduces the total cost of ownership over time.

Not Negotiating Purchase Price

Many Canadians accept the listed price of a vehicle without negotiation, leading to higher financing amounts. Even small reductions in purchase price can significantly lower total loan cost and interest. Buyers who skip negotiation may pay more than necessary. In 2026, competitive inventory levels provide more opportunities to negotiate. Taking time to discuss pricing and explore incentives can result in meaningful savings. This approach helps reduce both upfront cost and long-term financial commitment.

Trading In Too Frequently

Frequent vehicle upgrades can lead to repeated financing cycles and increased debt. Canadians who trade in vehicles every few years often accumulate higher overall costs due to depreciation and interest. Each new loan resets the financial timeline, making it difficult to build equity. In 2026, holding onto vehicles longer has become a more practical strategy. Extending ownership reduces total expenses and allows buyers to benefit from paid-off vehicles. This approach improves financial stability and long-term value.

Ignoring Maintenance Costs

Maintenance costs vary widely between vehicles, but many buyers overlook them when financing. Luxury or performance vehicles often require more expensive servicing and parts. Canadians who focus only on purchase price may face higher ongoing expenses. In 2026, reliability and maintenance costs are key factors in total ownership. Choosing vehicles with strong reliability ratings helps reduce unexpected expenses. Factoring maintenance into decisions leads to better long-term financial outcomes.

Not Considering Total Ownership Strategy

Many Canadians approach car purchases without a long-term strategy, focusing only on immediate needs or preferences. This can lead to decisions that increase costs over time. Financing terms, vehicle choice, and usage patterns all affect overall affordability. In 2026, a strategic approach that accounts for total ownership cost yields better results. Buyers who plan ahead and align their choices with long-term goals avoid common regrets. This includes selecting appropriate loan terms, reliable vehicles, and realistic budgets.

19 Things Canadians Don’t Realize the CRA Can See About Their Online Income

Earning money online feels simple and informal for many Canadians. Freelancing, selling products, and digital services often start as side projects. The problem appears at tax time. Many people underestimate how much information the CRA can access. Online platforms, banks, and payment processors create detailed records automatically. These records do not disappear once money hits an account. Small gaps in reporting add up quickly.

Here are 19 things Canadians don’t realize the CRA can see about their online income.