In a time of fluctuating interest rates, shifting markets, and evolving tax rules, financially savvy Canadians are making calculated moves to protect and grow their money. From optimizing investment strategies to reducing everyday costs, these steps are designed to create stability while positioning for long-term gains. Here are 25 financial moves smart Canadians are making right now:

Locking In Mortgage Rates

With interest rates still in flux, many Canadians are locking in fixed-rate mortgages to protect against future hikes. While variable rates can offer savings in certain markets, locking in now provides predictable monthly payments and shields homeowners from sudden increases. Some are even refinancing existing loans to secure more favorable terms before rates potentially climb. This move offers stability in household budgeting and can make long-term planning easier. For those with substantial mortgage balances, locking in a competitive rate today could save thousands over the life of the loan.

Maximizing TFSA Contributions

The Tax-Free Savings Account remains one of the most flexible and powerful tools in a Canadian’s wealth-building arsenal. Savvy investors are making sure to contribute up to the annual limit, and for those with unused room from previous years, catching up can have significant tax-free growth potential. TFSAs can hold everything from high-interest savings to stocks and ETFs, and all earnings inside remain untaxed, even upon withdrawal. By filling this account early in the year, Canadians allow investments more time to grow.

Paying Down High-Interest Debt

With credit card interest rates often exceeding 20%, eliminating high-interest debt is one of the fastest, most guaranteed ways to improve financial health. Canadians are focusing on clearing these balances before aggressively investing, freeing up cash flow and reducing financial stress. Some use the avalanche method, which is tackling the highest rates first, while others prefer the snowball method for quick wins. Consolidation loans and low-interest balance transfers are also being used to manage repayment more efficiently.

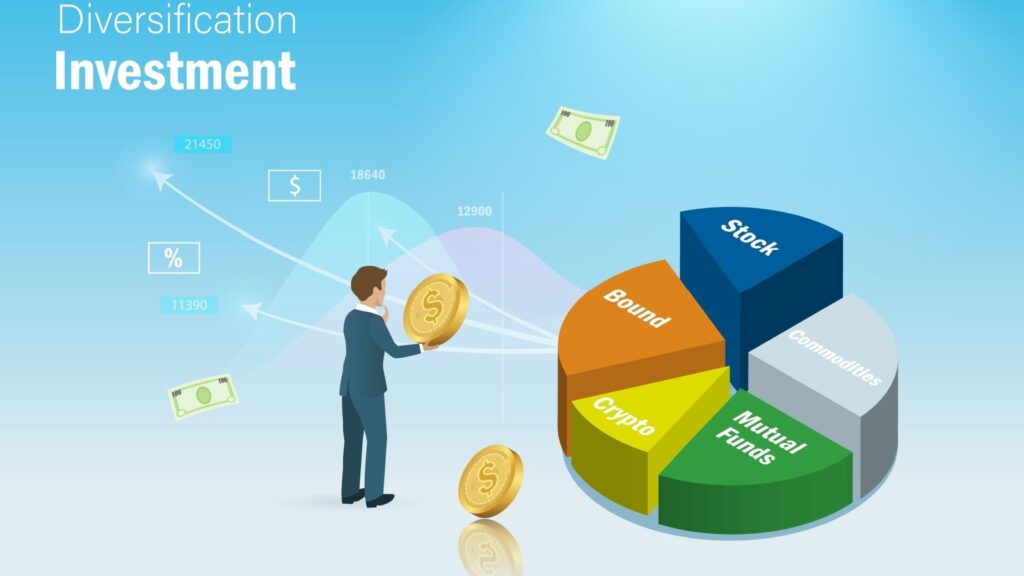

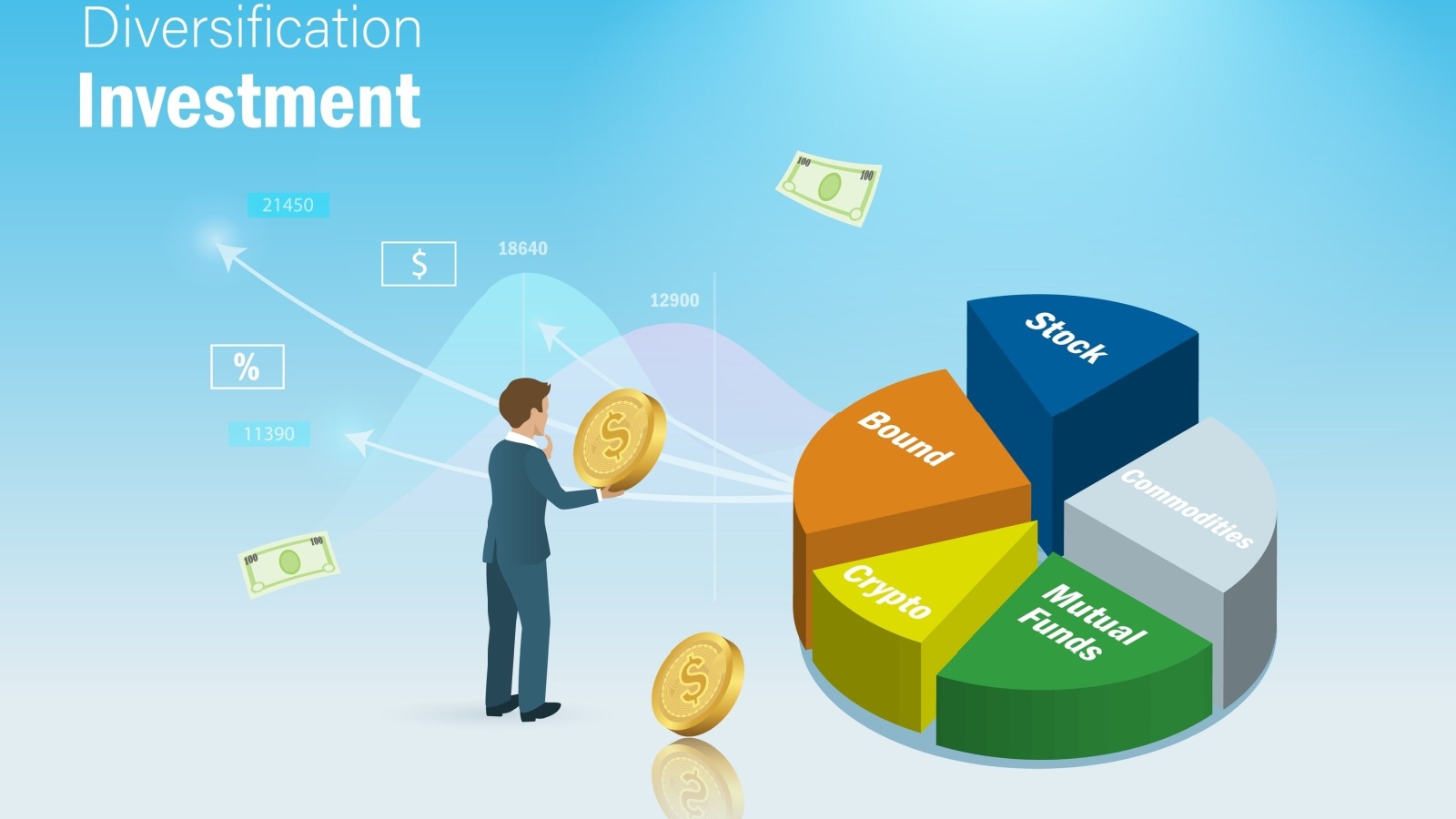

Diversifying Investment Portfolios

Market volatility has underscored the importance of diversification. Savvy Canadians are spreading their investments across asset classes, like stocks, bonds, real estate, and alternative assets, to balance risk and reward. Many are also looking beyond domestic markets to include international exposure, reducing reliance on a single economy, as regular rebalancing ensures portfolios stay aligned with personal goals and risk tolerance. This disciplined approach smooths out returns over time and prevents emotional decision-making during market swings.

Building Emergency Funds

Economic uncertainty makes a well-funded emergency savings account more valuable than ever. Canadians are aiming to keep at least three to six months’ worth of living expenses in a high-interest savings account, ensuring they can weather job loss, medical emergencies, or major home repairs without going into debt. A dedicated emergency fund provides financial protection and peace of mind, allowing investments to remain untouched during downturns. The security of knowing unexpected expenses won’t derail long-term goals is a cornerstone of smart financial planning.

Taking Advantage of Employer Matching Programs

Employer-sponsored retirement plans with matching contributions are essentially free money. Canadians are ensuring they contribute at least enough to receive the full match, maximizing this benefit. Whether it’s a group RRSP, defined contribution plan, or pension enhancement, the additional contributions compound significantly over time. By treating the employer match as a non-negotiable part of their compensation, workers effectively give themselves an instant raise. Those who combine this with regular personal contributions are building retirement security at an accelerated pace without increasing their financial burden.

Investing in Low-Cost Index Funds

High management fees can quietly erode investment returns over decades. Canadians looking to optimize long-term growth are turning to low-cost index funds and ETFs, which track broad market performance at a fraction of the cost of actively managed funds. These vehicles offer diversification, transparency, and historically strong performance over time, and by keeping fees low, more of each year’s gains stay invested, allowing compounding to work more efficiently. For many, this simple shift in strategy could result in tens of thousands of additional wealth over the course of a career.

Reviewing and Updating Insurance Coverage

Life circumstances change as homes are upgraded, families grow, and incomes shift, prompting smart Canadians to review their insurance policies to ensure coverage matches current needs. This includes life, home, auto, and disability insurance, while some are also increasing coverage to protect against inflation, and others are trimming unnecessary policies to save money. Bundling services or shopping for new quotes can reduce premiums without sacrificing protection.

Negotiating Better Rates on Bills

From cell phone plans to internet service and even insurance premiums, many Canadians are cutting costs simply by asking. Providers often have unadvertised discounts or loyalty offers, but they typically go to customers who request them. By shopping around, mentioning competitor rates, or timing negotiations near contract renewals, Canadians can save hundreds annually. The money saved on recurring bills can be redirected toward investments, debt repayment, or other financial goals, as negotiating is considered a habit that compounds into meaningful savings over time.

Leveraging Tax Credits and Deductions

Canada’s tax system offers numerous opportunities to reduce taxable income, from RRSP contributions and medical expense deductions to credits for tuition, charitable donations, and home energy upgrades. Smart Canadians track eligible expenses throughout the year and sometimes consult tax professionals to ensure nothing is missed. The savings can be significant, and reinvesting them creates a compounding effect on wealth. Understanding and applying tax advantages turns a once-a-year obligation into a powerful tool for long-term financial growth.

Automating Savings and Investments

Consistency is key to wealth building, and automation makes it effortless. Canadians are setting up pre-authorized transfers to savings accounts, TFSAs, RRSPs, and investment portfolios on payday, ensuring they pay themselves first. This removes the temptation to spend before saving and turns good intentions into tangible progress. Dollar-cost averaging also helps smooth market volatility, as investments are purchased regularly over time. Automation allows wealth to grow quietly in the background while freeing mental energy for other priorities.

Taking Advantage of High-Interest Savings Accounts

With interest rates higher than in recent years, high-interest savings accounts (HISAs) have become more attractive. Canadians are moving emergency funds, short-term savings, and even some idle cash into HISAs to earn better returns without risking principal. While the gains may seem modest compared to investments, they are also risk-free and liquid, which is perfect for funds that might be needed quickly. Combining safety, accessibility, and higher-than-average returns, these accounts are a smart home for money that’s waiting for its next purpose.

Delaying Large Purchases

In an era of inflation and fluctuating supply chains, Canadians are pressing pause on big-ticket buys unless truly necessary. Delaying gives time to save cash, research options, and take advantage of potential price drops or seasonal sales. Avoiding impulse purchases also reduces the risk of financing at high interest rates. This patience can translate into significant savings and less financial strain, allowing funds to be redirected toward higher priorities like investing, debt reduction, or home improvements that add lasting value.

Rebalancing Investment Portfolios

Market movements can throw asset allocations out of balance, increasing risk unintentionally. Canadians are reviewing portfolios at least annually, selling overweight positions and reinvesting in underrepresented areas to restore the desired mix. This disciplined approach locks in gains from outperforming assets while keeping risk aligned with personal goals. Rebalancing also forces investors to buy low and sell high, a principle that supports long-term returns.

Exploring Side Income Streams

With the cost of living rising, many Canadians are creating extra income through side hustles, freelancing, or monetizing hobbies. Whether it’s tutoring, consulting, pet sitting, or selling products online, these ventures provide financial breathing room and extra funds for savings or debt repayment. The flexibility of side income means it can adapt to changing schedules and goals, and in some cases, it evolves into a full-time business.

Contributing Early to RRSPs

Instead of waiting until the RRSP deadline, Canadians are making contributions earlier in the year to give investments more time to grow. This strategy maximizes compounding potential and spreads out contributions to ease cash flow, while RRSP contributions also reduce taxable income, often resulting in refunds that can be reinvested. For higher earners, early contributions combined with strategic withdrawals in lower-income years create powerful tax advantages over a lifetime.

Shopping Secondhand

Canadians are embracing thrift stores, online marketplaces, and consignment shops to save on clothing, furniture, and household items. Beyond the environmental benefits, buying secondhand can cut costs dramatically without sacrificing quality, especially for children’s items or tools used infrequently. The savings from this habit can be redirected into investments or other financial priorities, proving that frugality and style can coexist. In a high-inflation environment, secondhand shopping is both a budget-friendly and sustainable choice.

Reviewing Subscription Services

Streaming platforms, software, gym memberships, etc., are subscriptions that can quietly drain hundreds each year. Canadians are auditing recurring expenses and canceling those they rarely use or can replace with free alternatives. Even trimming just a few services can free up funds for more impactful uses. Setting reminders before free trials end and tracking renewals prevents accidental charges, as this small but consistent habit keeps budgets lean without sacrificing quality of life.

Increasing Retirement Contributions

For those able to, bumping up retirement savings by even 1-2% can make a significant difference over time. Canadians are taking advantage of salary increases, bonuses, or reduced expenses to boost RRSP or TFSA contributions without feeling the pinch. The earlier these contributions are made, the more time they have to compound, creating a larger nest egg with relatively little extra effort. Incremental increases are a low-pain, high-gain strategy for securing long-term financial independence.

Selling Unused Items for Cash

Decluttering homes isn’t just about creating space, but it also offers a way to generate extra income. Canadians are selling unused clothing, electronics, tools, and collectibles through online platforms or local consignment stores, and the cash earned can be applied to debt, added to savings, or reinvested. This habit not only improves living environments but also turns forgotten possessions into financial resources, making it a double win.

Keeping Credit Utilization Low

Credit scores impact everything from loan approvals to interest rates, and one key factor is credit utilization, which is the percentage of available credit being used. Canadians aiming for top scores keep utilization below 30%, pay off balances regularly, and request higher limits when appropriate. This not only improves borrowing terms but also creates a financial safety net, as a strong credit profile can save thousands over a lifetime in reduced interest costs.

Taking Advantage of Government Grants

From the Canada Education Savings Grant for RESP contributions to home energy retrofit incentives, Canadians are tapping into government programs that provide financial boosts. These grants often require proactive applications or specific eligibility steps, but the payoff can be substantial. By combining personal contributions with matching or subsidized funds, savers accelerate progress toward education, home improvement, or retirement goals without extra strain on their budgets.

Meal Planning to Cut Grocery Costs

Food prices continue to climb, prompting Canadians to plan meals strategically to avoid waste and reduce impulse purchases. Creating weekly menus based on sales, bulk buys, and seasonal produce helps stretch grocery budgets further, and cooking at home also costs less than frequent dining out, freeing funds for other priorities. Over time, the savings from consistent meal planning can be significant without compromising on nutrition or variety.

Timing Major Home Renovations Wisely

Instead of jumping into renovations during peak demand, Canadians are timing projects for off-season periods when contractors may offer better rates. They are also getting multiple quotes, sourcing materials strategically, and focusing on upgrades that boost resale value or energy efficiency. Thoughtful planning not only saves money upfront but also maximizes the long-term return on investment, making home improvements a smarter financial move.

Staying Informed About Economic Trends

Smart Canadians keep an eye on interest rates, inflation data, and market movements to make timely financial decisions. This doesn’t mean reacting to every headline, but understanding how broader trends may impact mortgages, investments, or employment. Staying informed allows them to adjust strategies proactively, whether that is locking in loans, rebalancing portfolios, or seeking new income opportunities, as knowledge remains a powerful tool in protecting and growing wealth, especially in uncertain times.

21 Products Canadians Should Stockpile Before Tariffs Hit

If trade tensions escalate between Canada and the U.S., everyday essentials can suddenly disappear or skyrocket in price. Products like pantry basics and tech must-haves that depend on are deeply tied to cross-border supply chains and are likely to face various kinds of disruptions

21 Products Canadians Should Stockpile Before Tariffs Hit