In a time when economic uncertainty makes riskier investments feel like walking a tightrope without a net, Canadians are finding ways to grow wealth with steady, reliable strategies. These approaches aren’t about chasing overnight riches, but about building lasting financial security through consistency, smart planning, and informed choices. Here are 25 proven ways to grow wealth in Canada without huge risk:

Max Out Your TFSA Contributions

The Tax-Free Savings Account (TFSA) is one of Canada’s most powerful low-risk wealth-building tools. By contributing the annual maximum and investing in safe assets like GICs, index funds, or blue-chip dividend stocks, your gains are entirely tax-free. Over time, the combination of steady growth and compounding can create significant wealth without exposing you to high volatility. The flexibility to withdraw funds without penalties also makes it an ideal safety net.

Invest in Blue-Chip Dividend Stocks

Blue-chip dividend-paying stocks, such as Canadian banks or major utilities, provide stable returns and regular income. These companies have proven track records, strong balance sheets, and the resilience to withstand economic downturns. By reinvesting dividends, your portfolio compounds over time, boosting long-term gains. While not completely risk-free, blue chips tend to be far less volatile than smaller growth stocks, and they also offer the comfort of steady payouts that can supplement retirement income or be reinvested for faster wealth accumulation.

Leverage the FHSA for Dual Benefits

The First Home Savings Account (FHSA) is one of Canada’s newest financial tools, combining the benefits of an RRSP and a TFSA. Contributions are tax-deductible, and withdrawals for a qualifying first home are tax-free. Even if you don’t plan to buy a home soon, you can invest within the FHSA and grow funds tax-free until you decide, or transfer the balance to your RRSP without affecting your contribution room. This dual-purpose structure makes it a low-risk, high-reward option for both future homeowners and long-term investors.

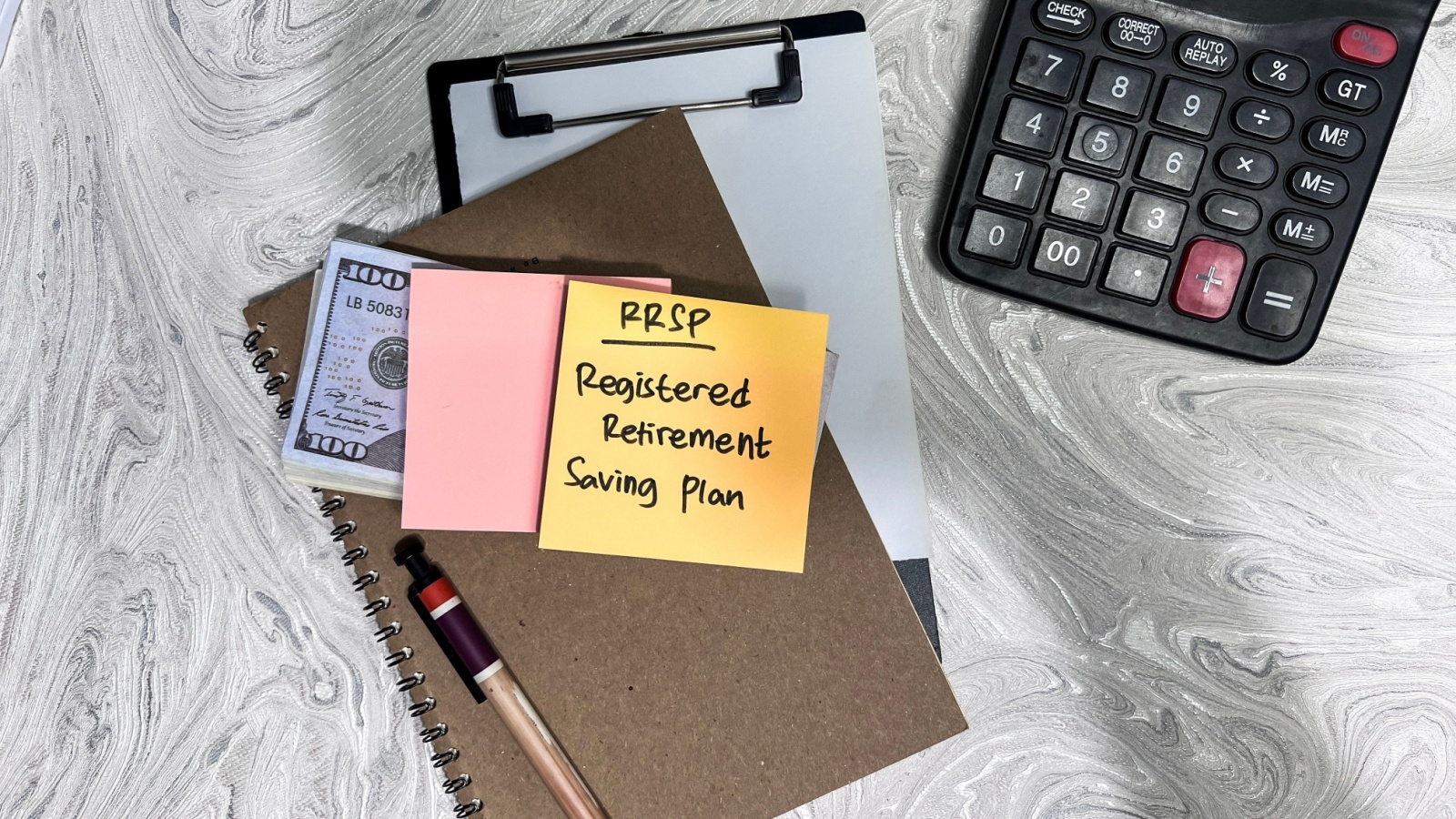

Take Advantage of RRSP Tax Benefits

The Registered Retirement Savings Plan (RRSP) helps you grow wealth while lowering your taxable income. Contributions are tax-deductible, and investments inside the plan grow tax-deferred until withdrawal, often at a lower tax rate in retirement. This makes RRSPs ideal for long-term, low-risk wealth building, and many Canadians use them to hold safe investments like bonds, conservative ETFs, or balanced funds. By reinvesting your tax refunds into your RRSP each year, you compound your growth even faster, and with discipline, this account can become a cornerstone of a secure retirement strategy.

Ladder Your GIC Investments

Guaranteed Investment Certificates (GICs) are one of the safest investment options in Canada. A GIC ladder strategy, which is investing in multiple GICs with staggered maturity dates, ensures you always have one coming due to reinvest at potentially higher rates. This balances liquidity and returns while minimizing interest rate risk. Your principal is guaranteed, and the predictable income makes budgeting easier. While returns are modest compared to riskier investments, GICs offer peace of mind and steady growth, making them an excellent foundation for a low-risk wealth-building plan.

Reinvesting Dividends Automatically

Many Canadians are building wealth steadily by enrolling in Dividend Reinvestment Plans (DRIPs). Instead of taking cash payouts from dividend-paying stocks, they reinvest them to buy more shares automatically, often without brokerage fees, which compounds returns over time without extra effort. DRIPs are especially powerful for blue-chip Canadian companies with a strong history of increasing payouts. By letting dividends generate more dividends, investors create a snowball effect that grows even during market slowdowns.

Renting Out Unused Space

Homeowners across Canada are monetizing basements, spare rooms, garages, and even parking spots. With housing shortages in major cities and high rental demand in smaller towns, unused space can bring in hundreds or even thousands per month. Platforms like Airbnb, Neighbor, or local classifieds make it easy to find short- or long-term tenants. Many Canadians are using this extra income to pay down mortgages faster or boost savings without dipping into their salaries, which is a wealth-building move that turns idle property into consistent cash flow.

Investing in Low-Fee Index Funds

Index funds and ETFs remain one of the most reliable, low-risk investment vehicles for Canadians who want long-term growth without high management fees. By tracking broad market indexes like the S&P/TSX Composite or S&P 500, they provide instant diversification across dozens or hundreds of companies. Lower fees mean more of your returns stay in your pocket, and compounding does the rest over time. This passive approach has been especially popular among young investors who want consistent returns without the stress of stock picking or day trading.

Leveraging RRSP Contribution Room

Savvy Canadians make full use of their Registered Retirement Savings Plan (RRSP) contributions each year to lower taxable income while growing investments tax-deferred. By strategically contributing before the tax deadline, they can often secure a significant refund, which can then be reinvested. Many also use RRSPs to hold dividend-paying stocks, ETFs, or bonds, letting compounding work more efficiently. The key is consistency and maxing out or at least steadily increasing contributions each year, and over decades, RRSP growth can create a sizable retirement fund without needing risky or speculative investments.

Building Emergency Funds Before Investing Heavily

Before committing large sums to the stock market or real estate, many Canadians prioritize building an emergency fund, which is typically three to six months’ worth of living expenses. This safety net prevents them from having to sell investments during downturns or take on high-interest debt during unexpected crises. Emergency savings are often kept in high-interest savings accounts or GICs for easy access and guaranteed returns. This foundational step reduces financial stress, creates stability, and ensures that short-term financial setbacks don’t derail other wealth-building strategies.

Building Multiple Streams of Income

Smart Canadians are reducing financial risk by creating multiple income sources instead of relying solely on one job. This might mean combining a full-time salary with freelance work, a small online store, dividend-paying investments, or rental income. By diversifying their income sources, they create a safety net against job loss or market downturns, and even if one stream slows, others can keep cash flow steady. Over the years, these extra earnings can be reinvested, accelerating wealth growth without relying on high-risk ventures, which offers stability, flexibility, and a better sense of control over long-term financial security.

Building a Dividend Income Stream

Many Canadians are leveraging dividend-paying stocks and ETFs to create a steady income stream without taking on excessive risk. By focusing on companies with strong track records of consistent dividend payouts, and ideally, dividend growth, investors can generate reliable cash flow while also benefiting from potential capital appreciation. Reinvesting dividends through DRIPs (Dividend Reinvestment Plans) compounds returns faster, turning modest investments into substantial long-term wealth. This approach works particularly well in Canada thanks to the favorable tax treatment of eligible dividends, making it a smart, sustainable strategy for those seeking passive income and long-term financial security

Investing in Dividend-Growth Stocks

Dividend-growth stocks offer a steady income stream and long-term appreciation, making them a popular choice for cautious Canadian investors. By focusing on companies with a strong track record of increasing dividends annually, often in sectors like banking, utilities, and telecommunications, you benefit from both reliable cash flow and potential capital gains. Reinvesting those dividends accelerates compounding, further boosting wealth over time, and unlike speculative plays, dividend growers often weather market volatility better, providing peace of mind. This strategy works particularly well in Canada, where many blue-chip companies have decades-long dividend histories.

Using High-Interest Savings Accounts (HISAs)

High-interest savings accounts are a low-risk, accessible way for Canadians to grow their money without exposure to market swings. Many online banks offer rates significantly higher than traditional brick-and-mortar institutions, and your funds remain fully liquid. With no risk to principal, thanks to CDIC insurance for most deposits, HISAs are ideal for short-term goals or emergency funds. Some Canadians strategically use promotional rates and switch accounts every few months to maximize returns. While you won’t get rich overnight, HISAs protect your purchasing power and provide a safe, steady return that can outpace traditional savings accounts by a wide margin.

Investing in Chip REITs

Real Estate Investment Trusts (REITs) let Canadians access the real estate market without buying property directly, reducing barriers to entry. Blue-chip REITs, with strong balance sheets, diversified property portfolios, and consistent dividend payouts, are particularly attractive for low-risk wealth building. These trusts often invest in commercial, industrial, or residential properties, generating income through rents. Because they trade like stocks, you can easily buy and sell units, maintaining liquidity. In Canada, some REITs have delivered decades of reliable income and steady growth, making them a practical way to gain real estate exposure while avoiding the headaches of direct property management.

Use RRSP Spousal Contributions for Long-Term Tax Benefits

Spousal RRSPs can be a smart way to minimize taxes while preparing for retirement. By contributing to your spouse’s RRSP, the higher-income earner receives the immediate tax deduction, while withdrawals in retirement can be taxed at the lower-income spouse’s rate. This income-splitting advantage can significantly reduce overall taxes in retirement, making it particularly useful for couples with income disparities, allowing both partners to grow retirement savings more evenly. By strategically using spousal contributions, Canadians can protect wealth, enhance after-tax income, and reduce financial strain in later years, all with minimal investment risk.

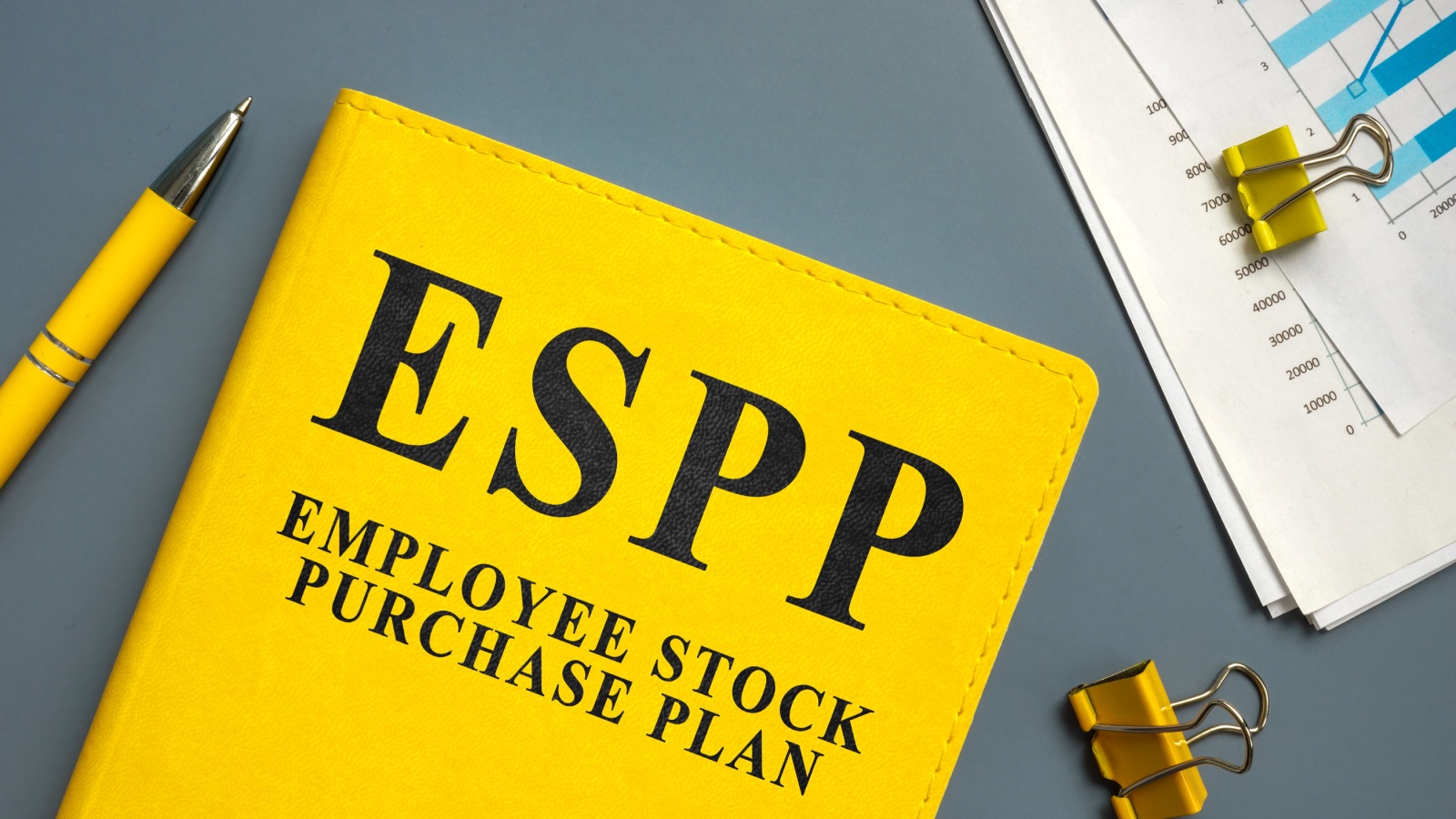

Participating in an Employee Stock Purchase Plan (ESPP)

Many Canadian employers offer Employee Stock Purchase Plans, allowing staff to buy company shares at a discount, often through automatic payroll deductions. This can be an excellent low-risk wealth-building tool, especially if the employer is stable and profitable. The built-in discount provides instant equity growth, and any dividends can be reinvested to further compound returns. Over time, consistently contributing to an ESPP can create substantial wealth with minimal effort. The key is diversification, and avoiding letting company stock dominate your portfolio to reduce risk.

Paying Down High-Interest Debt First

Eliminating high-interest debt, especially from credit cards, can be one of the most powerful, risk-free ways to build wealth in Canada. Every dollar you put toward paying off a 19% interest card effectively earns you a 19% return, far exceeding most investment yields. Many Canadians adopt the debt avalanche method, targeting the highest-interest balances first while making minimum payments on others. Once the debt is gone, those freed-up payments can be redirected into savings or investments. This approach not only boosts net worth but also improves credit scores, reduces financial stress, and creates more flexibility for future wealth-building moves.

Buying Inflation-Resistant Assets

Inflation erodes purchasing power, but certain assets, like gold, commodities, real estate, and inflation-protected bonds, tend to hold or increase their value when prices rise. Many Canadians are strategically allocating a portion of their portfolios to these inflation-resistant investments as a safeguard. Real estate often appreciates alongside inflation, while gold serves as a hedge during economic uncertainty. Government-issued Real Return Bonds also adjust payouts with inflation, protecting fixed-income streams. By holding a diversified mix of these assets, investors can shield their wealth from erosion while still participating in market growth, which ensures stability through both economic booms and downturns.

Building a Side Income Stream

Creating a reliable side income, through freelancing, consulting, tutoring, or small-scale e-commerce, offers Canadians an additional path to grow wealth without heavy financial risk. The key is choosing a skill or activity that requires minimal upfront investment and fits your schedule. Side income not only increases cash flow but also allows you to invest more aggressively, pay down debt faster, or save for major goals. Many Canadians start small, reinvesting profits into expanding their side venture. Over time, a well-managed side hustle can become a significant source of financial security, reducing dependence on a single paycheck and enhancing long-term stability.

Investing in REITs Instead of Direct Real Estate

Real Estate Investment Trusts (REITs) allow Canadians to invest in income-generating property portfolios, such as apartments, commercial buildings, and industrial spaces, without the hassle of being a landlord. REITs pay out a portion of rental income as dividends, providing regular cash flow, and they are traded like stocks, so they’re more liquid than physical properties and can be added to registered accounts for tax advantages. This makes REITs a practical way to diversify into real estate without needing hundreds of thousands in capital or dealing with tenants and maintenance.

Automating Savings and Investments

Setting up automatic transfers to savings accounts, RRSPs, or investment platforms is a proven way to grow wealth without relying on willpower. By treating these transfers like a fixed monthly expense, Canadians ensure that investing happens before spending. Apps and robo-advisors make this even easier, rounding up purchases or scheduling contributions on paydays. This “pay yourself first” approach removes emotional decision-making, smooths out market volatility through dollar-cost averaging, and builds consistent progress toward financial goals over years, often without the saver even noticing the gradual wealth accumulation.

Joining Credit Unions for Better Rates

Credit unions in Canada often provide lower loan rates, higher savings account interest, and fewer fees compared to big banks. Members benefit from being part-owners of the institution, which means profits are reinvested into better services rather than shareholder dividends. For mortgages, credit unions sometimes offer more flexible terms and competitive fixed or variable rates, and over a lifetime, these savings can add up significantly. Many Canadians also appreciate the local, community-focused approach of credit unions, which often translates to more personalized financial advice and support for long-term wealth growth.

Capitalizing on Employer Benefits and Matching Programs

Some Canadian employers offer Registered Pension Plans (RPPs) or RRSP matching programs, essentially free money for employees who contribute. Failing to take full advantage leaves potential wealth on the table. By contributing enough to maximize matching, Canadians instantly boost their retirement savings while enjoying tax advantages. Additional benefits like stock purchase plans, profit-sharing, and wellness stipends can also be redirected toward long-term savings. Over decades, employer-assisted contributions can compound into hundreds of thousands in extra retirement funds without any additional financial strain on the individual.

Prioritizing Long-Term, Low-Volatility Assets

Many Canadians avoid chasing risky, high-volatility investments in favor of steady, proven performers like blue-chip stocks, government bonds, and dividend aristocrats. While these may not deliver overnight riches, they protect capital during downturns and provide reliable growth over time. The strategy is built on patience, diversification, and the understanding that avoiding major losses is just as important as making gains. By focusing on assets with consistent returns and lower risk profiles, Canadians create a stable financial base that can support more aggressive investments later if desired.

21 Products Canadians Should Stockpile Before Tariffs Hit

If trade tensions escalate between Canada and the U.S., everyday essentials can suddenly disappear or skyrocket in price. Products like pantry basics and tech must-haves that depend on are deeply tied to cross-border supply chains and are likely to face various kinds of disruptions

21 Products Canadians Should Stockpile Before Tariffs Hit