Canadian retail aisles are starting to tell a different story in 2026. The changes are not always dramatic, but they are visible in small details: more discount shelving, more private-label space, more health cues, more screens, and more products designed around convenience rather than abundance. Together, these shifts show how retailers are responding to tighter household budgets, changing food habits, labour pressures, theft concerns, and the growing role of digital shopping.

These 20 store aisle changes reveal how Canadian retail is moving away from the old model of wide choice at any cost and toward a more calculated mix of value, speed, data, wellness, and control.

Bigger Private-Label Displays Are Moving to the Centre

Store brands are no longer being tucked away as the cheaper backup option. In many Canadian grocery aisles, private-label products now sit at eye level, appear on endcaps, and compete directly with national brands in packaging, flavour variety, and premium positioning. A shopper looking for crackers, frozen pizza, coffee, or household cleaners may now see the retailer’s own brand presented as the practical default rather than the budget compromise.

This shift reflects a more intentional value strategy. As food prices remain elevated, Canadian shoppers are mixing premium purchases with cheaper staples, and retailers have a strong incentive to promote products they control more closely. The aisle tells the story: store brands are being treated less like “no-name” substitutes and more like loyalty-building tools. For families comparing baskets week after week, the expanded private-label section signals that affordability is becoming a central battleground.

Discount Banners Are Influencing Regular Store Layouts

The discount grocery format is shaping more than just discount stores. Even conventional supermarkets are borrowing visual cues from hard-discount retail: simplified shelving, larger price callouts, fewer decorative touches, and prominent bulk or multi-buy displays. The result is an aisle that feels more focused on the deal than on browsing pleasure.

This is not accidental. Major Canadian retailers have been investing heavily in discount banners and renovations, especially as shoppers remain cautious about food costs. A standard supermarket may still carry premium products, but more space is being organized around “value zones” that mimic the look and logic of No Frills, Maxi, Food Basics, or FreshCo. When shoppers see bargain-style signage creeping into mainstream stores, it shows how deeply the discount mindset has entered Canadian retail.

More Endcaps Are Being Sold Like Media Space

Endcaps used to be simple promotional areas. In 2026, they increasingly function like in-store advertising inventory. A cereal display, a beverage cooler screen, or a personal-care feature may be tied to a brand campaign, loyalty data, seasonal timing, or a retailer’s digital media strategy. The aisle is becoming part shelf, part billboard.

This matters because retailers are no longer just selling products; they are also selling shopper attention. As retail media grows, physical stores are being pulled into the same data-driven marketing system as apps and websites. A shopper may think a product is on the aisle end because it is popular, but it may be there because the brand paid for high-traffic visibility. That change makes store layouts more strategic and less neutral than they appear.

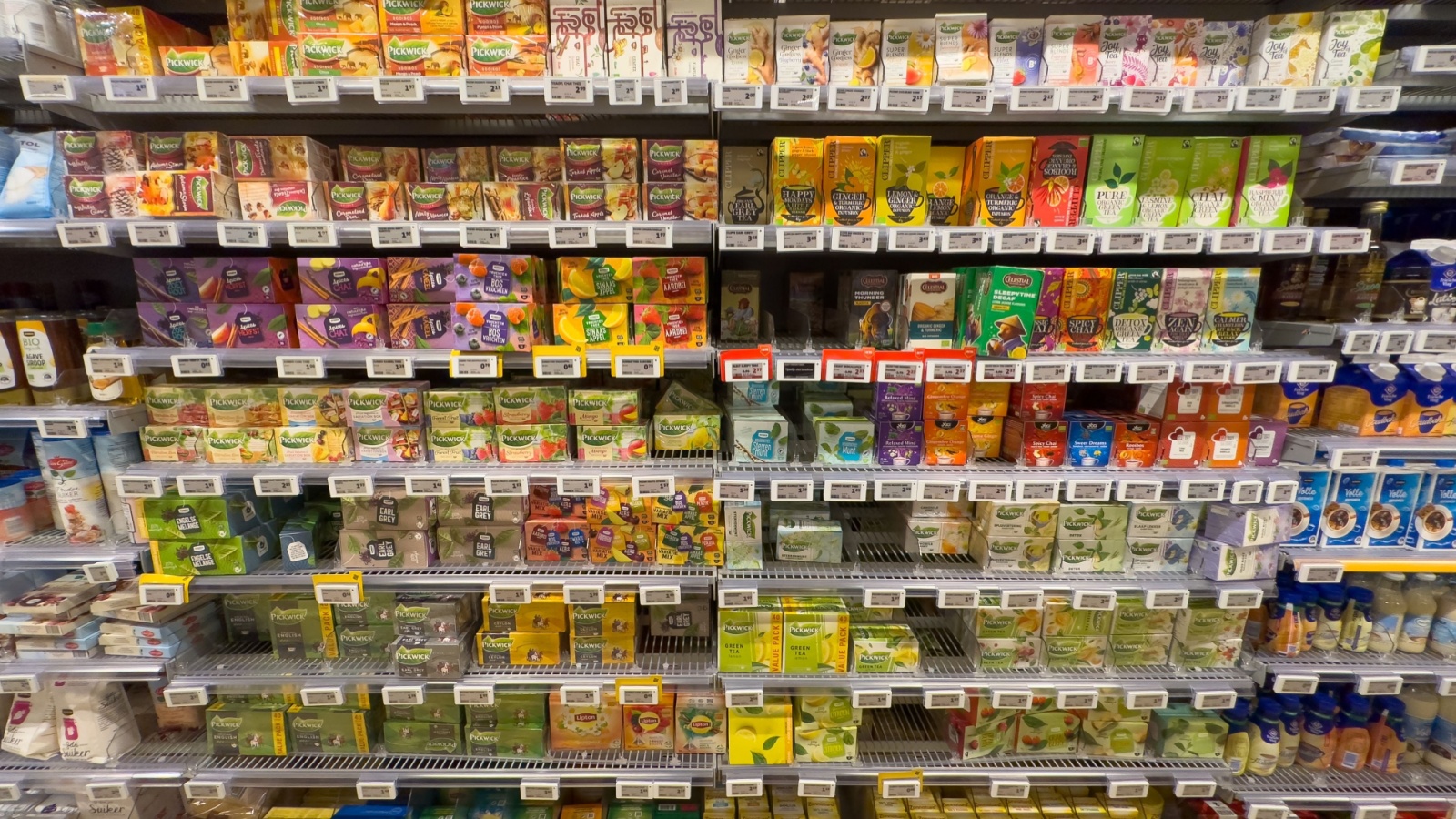

Digital Shelf Labels Are Replacing Paper Tags

Small electronic price tags are becoming more visible in Canadian retail, especially in stores trying to handle frequent price changes with fewer staff hours. Digital shelf labels can update prices quickly, reduce mismatches between shelf and checkout, and help stores manage promotions across thousands of items. In a busy grocery aisle, that can mean fewer paper tags taped over old prices.

The technology also raises questions. Shoppers are watching closely because faster price changes can feel unsettling when food budgets are already tight. Retailers often emphasize accuracy and efficiency, while critics worry about transparency and the possibility of more responsive pricing. Even if dynamic grocery pricing remains limited, the visual change is clear. Paper tags suggest fixed weekly pricing; digital labels suggest a store that can move faster than the old flyer cycle.

Front-of-Package Nutrition Symbols Are Changing Packaged Food Shelves

Packaged food aisles in Canada now carry more visible health information because front-of-package nutrition symbols became mandatory for many products high in saturated fat, sugars, or sodium. Shoppers browsing cereal, frozen meals, snacks, and prepared sauces may notice the warning-style symbols before they ever turn a package around to read the nutrition facts panel.

This changes the aisle in two ways. First, it makes some health information harder to ignore. Second, it may push manufacturers to reformulate products or adjust packaging to avoid standing out for the wrong reason. A bright snack package that once relied on flavour and fun may now share space with a prominent nutrition cue. For retailers, that makes shelf presentation more complicated: indulgence still sells, but health visibility is becoming part of the shopping experience.

Protein Claims Are Spreading Beyond the Fitness Aisle

Protein is no longer confined to powder tubs, energy bars, and sports nutrition shelves. In 2026, it is showing up across everyday grocery categories, including cereal, pasta, yogurt, snacks, drinks, and frozen meals. A shopper looking for a quick breakfast or lunch shortcut may see protein claims almost everywhere, even in products that once competed mainly on taste or convenience.

The appeal is straightforward. Protein signals fullness, energy, and value, which makes it useful for brands trying to justify higher prices. Retailers also benefit because protein-forward products often support premium pricing while still sounding practical. The aisle effect is noticeable: food categories are being reorganized around function, not just flavour. Shoppers are not only choosing between chocolate and vanilla anymore; they are choosing between “regular,” “high protein,” “high fibre,” and “better-for-you” versions of the same routine purchase.

Health and Wellness Space Is Expanding Near Everyday Essentials

Pharmacy, personal care, supplements, skin care, and wellness products are taking on a larger role in Canadian retail layouts. Stores are giving more attention to products tied to sleep, digestion, immunity, hydration, and self-care, often placing them close to daily essentials rather than isolating them in one back-corner aisle. The shift is especially visible in drugstores and grocery-pharmacy hybrids.

This follows consumer spending patterns. Health and personal care has been one of the stronger retail categories, even when households pull back elsewhere. A shopper who skips a new electronic gadget may still buy vitamins, skin care, pain relief, or wellness drinks. Retailers understand that wellness purchases can feel necessary rather than discretionary. As a result, the aisle increasingly blends medical need, beauty routine, and lifestyle aspiration into one larger retail zone.

Prepared Meals Are Taking Space From Raw Ingredients

Grab-and-go meals, ready-to-heat entrées, deli bowls, rotisserie counters, and frozen meal upgrades are becoming more important in store layouts. Instead of only pushing shoppers toward raw ingredients, retailers are carving out more space for products that solve the “what’s for dinner tonight” problem. The prepared food section is starting to look less like an add-on and more like a competitor to takeout.

This reflects a practical tension in Canadian households. Food prices are high, restaurant meals are expensive, and many families are short on time. A $12 prepared dinner may look costly beside dry pasta, but affordable beside delivery. Retailers are responding by placing convenient meals where tired shoppers will notice them quickly. The aisle change reveals a bigger truth: grocery stores are trying to capture spending that once went to restaurants, fast food, and meal delivery apps.

Frozen Aisles Are Becoming More Premium

The frozen aisle used to be heavily associated with basic vegetables, fries, pizza, and budget entrées. Now it is carrying more globally inspired meals, higher-quality desserts, protein-forward products, smoothie mixes, dumplings, seafood options, and single-serve convenience items. Freezer doors are being used to offer variety without requiring shoppers to cook from scratch.

This shift works because frozen food solves multiple problems at once. It can reduce waste, stretch meal planning, and offer convenience at a lower price than restaurant food. For retailers, frozen products also support longer shelf life than fresh prepared meals. The aisle’s appearance is changing accordingly: more premium packaging, more cuisine-specific options, and more “restaurant-style” language. A freezer section that once looked purely practical is becoming one of the clearest signs of Canadian shoppers balancing convenience with caution.

Ethnic and Global Foods Are Moving Out of the Specialty Corner

Global flavours are increasingly moving from small specialty sections into mainstream aisles. Sauces, noodles, spices, snacks, beverages, frozen dumplings, flatbreads, condiments, and rice varieties are appearing in broader sections instead of being treated as niche products. In many urban and suburban Canadian stores, this reflects the everyday reality of multicultural shopping baskets.

The aisle change is both demographic and commercial. Canada’s population growth has been strongly shaped by immigration, and retailers are responding to broader demand for familiar ingredients, cross-cultural meals, and restaurant-inspired flavours at home. A family may buy soy sauce, jerk seasoning, gochujang, paneer, tortillas, and maple syrup in the same trip. When these products move into the main flow of the store, it shows retailers are no longer treating diverse food preferences as side categories.

Smaller Pack Sizes Are Getting More Prominent

More shelves are showing smaller packages, single-serve formats, mini multipacks, and “right-sized” household options. These products can help shoppers manage cash flow, reduce waste, or serve smaller households, but they may also carry higher unit prices. The change is especially visible in snacks, beverages, meat, cheese, personal care, and cleaning products.

This is where the aisle can quietly reshape perception. A smaller package may look affordable because the sticker price is lower, even if the cost per gram or litre is higher. Retailers know many shoppers are focused on the total checkout bill, not only long-term value. With food prices still elevated, smaller formats let brands stay within psychologically acceptable price points. The growing presence of these packages shows how inflation pressure can change not just prices, but product design.

Unit Price Labels Are Becoming More Important Than Sale Tags

As package sizes shift and promotions get more complicated, unit pricing is becoming one of the most important details on the shelf. Shoppers comparing pasta sauce, laundry detergent, yogurt, or toilet paper may find that the biggest sale sign does not always represent the best deal. The real answer is often in the price per 100 grams, per litre, or per unit.

Retailers are under pressure to make value clear, but the aisle still rewards attention. Multi-buy offers, loyalty-only prices, and smaller packages can make direct comparisons harder. In 2026, the most informed shoppers are paying less attention to the loudest promotion and more attention to the small shelf label underneath. That shift reveals a more analytical kind of grocery shopping, where the aisle is not just a place to choose products but a place to decode pricing.

Loyalty-Only Pricing Is Reshaping Promotion Displays

More sale signs are being tied to loyalty cards, apps, digital coupons, or member pricing. The shelf may show one price for everyone and a lower price for customers who scan, load, tap, or identify themselves. This makes the aisle feel more personalized, but also more conditional. A deal is no longer always a deal unless the shopper is inside the retailer’s data system.

The change reflects the growing value of customer information. Loyalty programs help retailers understand buying patterns, target promotions, and strengthen repeat visits. For shoppers, they can deliver savings, but they also add friction. Someone without the app, the card, or the time to load offers may pay more for the same item. In-store pricing is becoming less universal, and the aisle is starting to mirror the segmented logic of online retail.

Self-Checkout Areas Are Being Redesigned for Control

Self-checkout zones are changing from open banks of machines into more supervised, controlled spaces. Some stores are adding gates, receipt checks, weight sensors, staff monitoring, item limits, or hybrid checkout formats. The goal is to keep speed while reducing errors, frustration, and theft. The front of the store is being redesigned as much for risk management as for convenience.

This reflects a broader debate in Canadian retail. Self-checkout promised efficiency, but many shoppers feel they are doing unpaid work while prices keep rising. Retailers, meanwhile, face concerns about shrink and store security. The new aisle-adjacent checkout layout shows the compromise: self-checkout is not disappearing, but the free-flowing version is being tightened. The result may feel less like a convenience zone and more like a monitored transaction area.

Locked Cases Are Appearing in More Everyday Categories

Security cases are no longer limited to razors, electronics, or expensive fragrances. In some stores, higher-theft everyday items such as baby formula, vitamins, skin care, laundry products, or over-the-counter medicines may be placed behind barriers or require staff assistance. That changes the rhythm of shopping, turning a quick grab into a request.

This is one of the clearest signs of rising retail crime concerns. Retailers are trying to reduce losses without driving away honest customers, but the customer experience suffers when basic items become harder to access. A locked shelf sends a message: the store is protecting inventory, not simply displaying it. For shoppers, it can feel frustrating or even uncomfortable. For retailers, it is a visible reminder that aisle design now has to balance trust, safety, and sales.

Alcohol Displays Are Adjusting to New Buying Patterns

Alcohol sections are changing in provinces where grocery access has expanded or where beverage retail rules continue to evolve. Beer, wine, ready-to-drink cocktails, and non-alcoholic alternatives are being merchandised with more care, often near snacks, entertaining items, or seasonal displays. In some stores, beverage aisles are becoming more like curated lifestyle zones.

The shift is not only about alcohol. Non-alcoholic beer, mocktails, sparkling beverages, and lower-sugar drinks are also gaining shelf attention as moderation becomes more mainstream. Retailers are responding to shoppers who may buy a craft beer for a barbecue, a zero-proof drink for a weekday dinner, and sparkling water for the same cart. Beverage aisles are becoming more segmented, reflecting changing social habits and a wider definition of “occasion-based” drinking.

Reusable and Low-Waste Products Are Taking More Shelf Space

Reusable bags, refillable containers, concentrated cleaners, compostable packaging, and low-waste household products are more visible than they were a few years ago. Canada’s restrictions on several single-use plastic items helped change checkout routines, but the aisle response goes further. Retailers now use sustainability cues as part of product positioning.

The effect is uneven. Some shoppers want less packaging, while others worry that eco-friendly options cost more or perform worse. Retailers are trying to meet both concerns by offering concentrated formats, refill pouches, and multipurpose products that promise savings as well as environmental benefits. A cleaning aisle with more refill systems and fewer bulky bottles signals a broader change: sustainability is moving from a corporate promise into shelf-level product design.

Food Waste Discounts Are Becoming More Visible

Marked-down produce, near-expiry meat, discounted bakery racks, and app-linked clearance sections are becoming more common. What once looked like a small back-of-store markdown area is now part of a larger value and waste-reduction strategy. Some shoppers actively plan around these sections, checking for discounted salad kits, yogurt, prepared meals, or produce boxes before paying full price elsewhere.

This change speaks to both affordability and environmental pressure. Retailers lose money when food is thrown out, while shoppers are looking for ways to stretch grocery budgets. Discounted near-expiry sections can help both sides when managed well. The aisle message is changing from “damaged goods” to “smart rescue.” For a family trying to reduce its bill, a bright clearance sticker can feel less like compromise and more like timing.

Click-and-Collect Picking Is Changing Aisle Organization

Online grocery orders are affecting physical store aisles even for people shopping in person. Wider paths, clearer category signs, backroom staging areas, and products arranged for faster picking all reflect the growth of click-and-collect and delivery. Staff with carts or handheld devices have become part of the regular shopping scene.

This creates a store that serves two customers at once: the person walking the aisle and the digital customer whose order is being assembled. Retailers must make products easy to find, scan, substitute, and restock. That can improve signage and inventory discipline, but it can also make aisles feel busier. The physical store is no longer just a showroom for shoppers; it is also a fulfillment centre, and that dual role is changing how space is used.

Seasonal Displays Are Arriving Earlier and Changing Faster

Seasonal aisles are turning over more quickly, with summer grilling, back-to-school, Halloween, holiday baking, and winter wellness displays appearing earlier than many shoppers expect. Retailers are using seasonal changes to create urgency, capture impulse purchases, and smooth out sales across longer periods. A patio display in spring or a Halloween candy shelf in late summer is not just decoration; it is calendar management.

This faster rotation reflects a more competitive retail environment. When shoppers are cautious, stores need reasons to make each visit feel timely. Seasonal displays also help retailers manage inventory, supplier promotions, and social media-driven demand. The aisle becomes a signal that the next spending occasion has already begun. For consumers, it can feel rushed; for retailers, it is a way to keep attention moving before budgets are spent elsewhere.

Fewer Duplicates Are Making Some Aisles Look More Curated

Some aisles are carrying fewer near-identical choices than they once did. Instead of five similar versions of the same product, stores may prioritize bestsellers, private-label options, premium choices, and value packs. This makes the shelf look cleaner, but it can also mean a favourite niche brand disappears without much notice.

The change is partly about efficiency. Retailers face pressure from logistics costs, labour shortages, inventory complexity, and limited shelf space. Every slow-moving product has to justify its place. A more curated aisle can make shopping easier, but it also concentrates power in the hands of retailers deciding what deserves visibility. In 2026, Canadian retail is not only shifting through what gets added to shelves, but through what quietly gets removed.

19 Things Canadians Don’t Realize the CRA Can See About Their Online Income

Earning money online feels simple and informal for many Canadians. Freelancing, selling products, and digital services often start as side projects. The problem appears at tax time. Many people underestimate how much information the CRA can access. Online platforms, banks, and payment processors create detailed records automatically. These records do not disappear once money hits an account. Small gaps in reporting add up quickly.

Here are 19 things Canadians don’t realize the CRA can see about their online income.